Decentralization of Credit Creation

The demise of free banking and the birth of central banks centralized the process of credit creation around the beginning of the 20th century. At the time this was a vast improvement over the "rogue" free banking landscape and must be appreciated as such, but as time progressed it has fostered concentration, increased leverage, and regulatory burden to counterbalance the natural tendencies of such a centralized system.

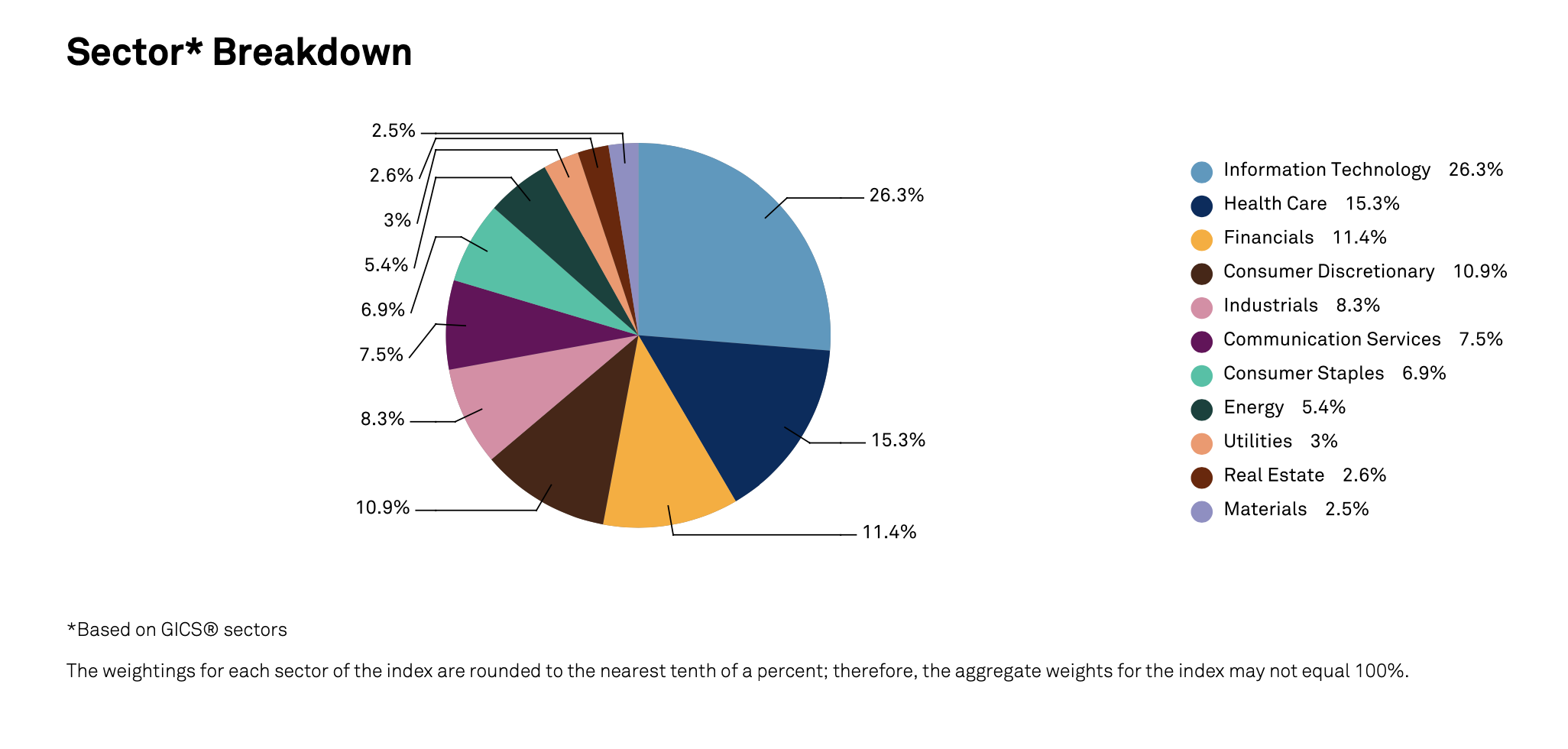

Even though banking today is still relatively fragmented as an industry, it has grown immensely relative to other industries and accounts for 11.4% of the S&P500 as of October 31st, 2022 as seen in the chart below (1). It has produced some of the biggest and most systemically important (read "too big to fail") institutions on the planet today. This increased scale & concentration in turn has necessitated regulatory oversight to manage the systemic risks and contributed to a gradual rise of the "barriers to entry" to the institutional credit market.

In Europe and the emerging markets, where credit markets are particularly bank-centric and public/institutional credit markets are less developed, credit creation is even more centralized than in the US where public debt markets are more developed.

The ever-increasing role of banks and more stringent bank capital requirements have led to bigger banks and standardization of credit products, in effect "raising the bar" for access (to either the bank's own balance sheet or that of the institutional credit markets they provide access to) to the detriment of small and medium-sized enterprises which are the driving force in most modern economies and essential to the very fabric of society.

Prof. Richard Werner (Oxford university professor in banking and finance) is a well-known public advocate of smaller and communal banking as a solution to many of the societal issues caused by the above trends, ranging from "too big to fail" institutions and regulatory overburden that we increasingly see.

We agree wholeheartedly with Prof. Werner's vision that smaller, decentralized, and regional/local credit creation could solve many of the problems that are endemic to our current banking system but this belief is in itself not enough to make it happen and/or work.

The issue is that such smaller financial institutions don't have the same access to institutional (cheap) funding as the larger institutions and therefore don't have the same economies of scale as their larger brethren, hence there is a natural tendency to end up with our current status quo.

It is clear however that the issues caused by this "status quo" will not be solved by those suffering the proverbial "Turkey's voting for Christmas" syndrome... The solution must lie in a grass-roots "re-design" of the financial primitive (utility) that we call banking. One that is not dependent on preferred access to capital markets and/or excessive leverage to pay for the largesse of its operators, regulators and/or owners. One that is so inherently stable and transparent that it requires minimal (regulatory) oversight and control. One that harnesses (blockchain) technology to provide immutable, auditable, and lasting alignment of incentives instead of over-dependence on manual/human control and oversight. Permissionless would be ideal but even in a permissioned form, we believe there is vast room for improvement over the current system.

At Florence.Finance we believe that blockchain technology can be harnessed to facilitate mutually beneficial cooperation between lenders & borrowers without having to lean on fractional reserve banking or securitization. We believe proving this thesis at scale with real-world borrowers & stablecoin lenders will yield one of many financial primitives that together form the future's decentralized and diverse financial system.

Our goal is to tackle real-world issues (use cases) that are currently underserved by the existing TradFi system to build trust & adoption in crypto whilst providing real-world value in an attempt to break the incestuousness of crypto to date.

References:

1) https://www.spglobal.com/spdji/en/indices/equity/sp-500/#overview