How are different platforms approaching RWA?

What are the top RWA protocols?

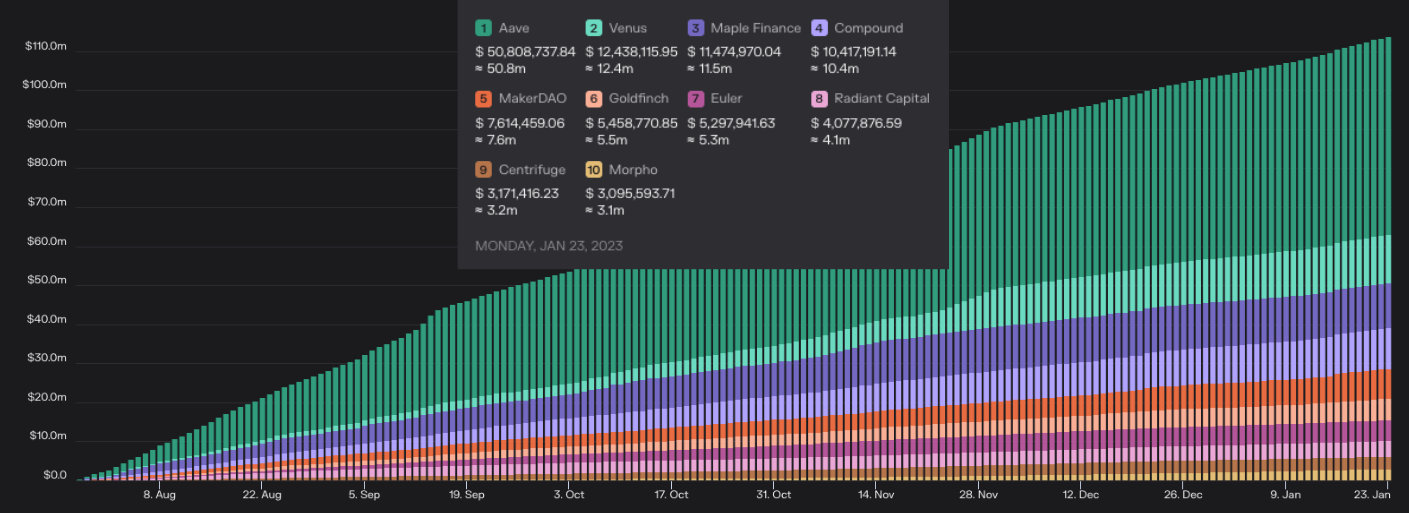

There have been many different approaches to Real World Assets (RWA) in the crypto space so far, the most notable efforts are from Centrifuge, MakerDAO, Maple, and Goldfinch. While the RWA narrative is still early we can see it starting to build momentum, if we take a look on Token Terminal at the top 10 lending protocols based on the cumulative 180 days of interest fees we see that four of them are RWA protocols (we will include MakerDAO seen as 57% of their revenue is from RWA).

MakerDAO

While MakerDAO is not an RWA project in and of itself they are still the largest contributor to RWA by far, as according to their Dune dashboard by @SebVentures they have now invested over $650m into various RWA projects.

So far the MakerDAO approach has been to invest varied amounts of DAI from their reserves into different protocols and let the revenues roll in. This strategy has been very effective from a revenue POV as RWA has gone from contributing 0.5% to overall DAO revenue to a staggering 57% over the last year, one of the only things up only in the bear market.

MakerDAO also brings a level of composability to the RWA space (this is DeFi after all) as they offer the ability to mint DAI against your selected Centrifuge lending positions, this allows you to borrow against your position and bring a degree of leverage to the space. While this may be seen as risky by some, due to Maker and Centrifuge's close-knit relationship in the case of liquidation MakerDAO themselves will liquidate the position and hold the Centrifuge tokenized RWA position until maturity to recoup their capital, this shows the degree of trust that MakerDAO has in the underlying credit on the Centrifuge platform.

Centrifuge

Recently Maker has collaborated with Centrifuge to facilitate their $150m investment into real-world loans sourced by BlockTower Capital, this collaboration solidifies Centrifuge's position as the largest pure RWA protocol in the market today with roughly $138m in the pools on their platform. Another up-only chart might we add, is there a pattern forming here? All signs are pointing to RWA being the next major narrative in DeFi, as real-world lending is a multi-trillion dollar market globally, to say we are early is an understatement.

So what is their approach to RWA and why are they the largest project so far?

Centrifuge uses tokenized real-world assets to bring crypto liquidity into the real world, "Tinlake" is their main dApp on the Ethereum blockchain and is the place to connect "asset originators" (borrowers) to investors (lenders). The investors providing the crypto liquidity to Tinlake can be protocols deploying treasuries like MakerDAO or KYC'd retail investors, but there are also liquidity pools on Maker that allows non-KYC retail investors to get exposure to the tokenized real-world assets. Centrifuge offers two different risk profile options to their users per pool, there are the Junior tokens (higher risk) and the Senior tokens (lower risk), thus allowing users to expose themselves to the degree of risk of their choice.

The Centrifuge team is highly experienced in the credit space as their previous venture was a very successful supply chain financing company that serviced 97 out of Fortune 100 companies in the USA, this experience is very likely driving Centrifuge's dominance in the market. Another driving factor for Centrifuge's dominance is its relationship with MakerDAO and Aave, both platforms offer access to Tinlake assets to their users and MakerDAO even lets users mint DAI against their Tinlake assets. This level of composability is helping attract large amounts of liquidity to Centrifuge and validating them as the leaders in the market.

Goldfinch

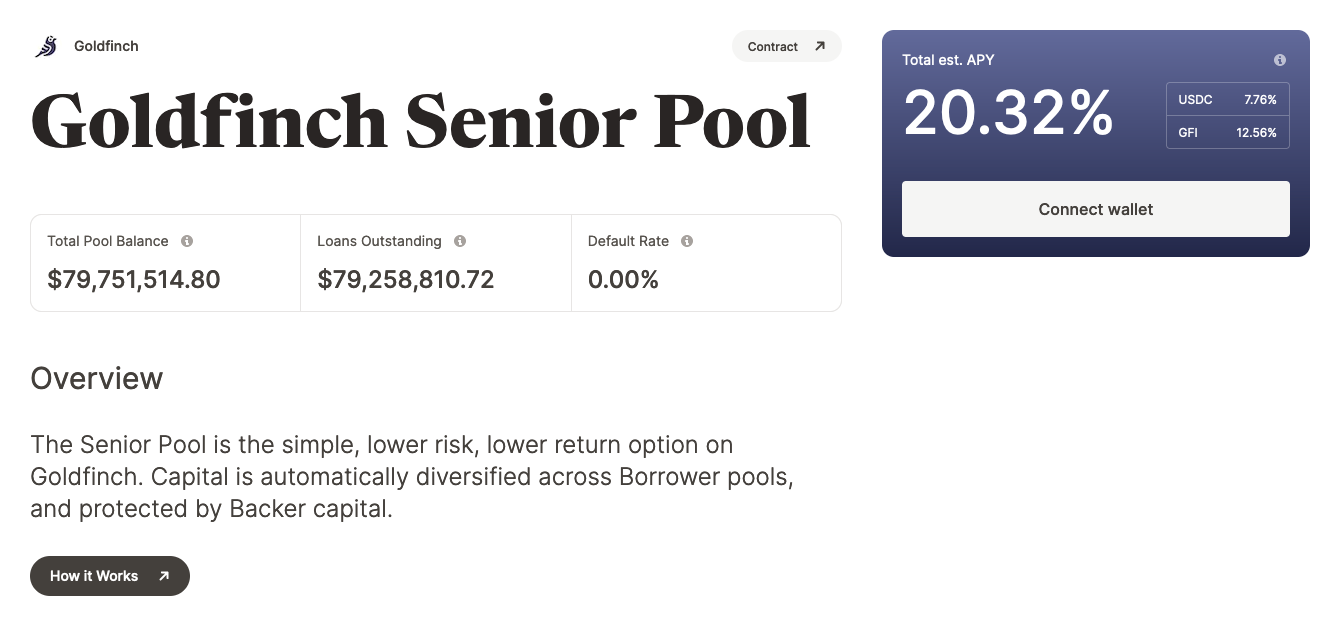

Goldfinch brings RWA to DeFi through undercollateralized lending to emerging markets and recently crossed $100m in active loans, and so far has a record of zero defaults. A great achievement on both fronts.

Goldfinch uses a combination of investors, borrowers, and auditors to create an ecosystem that offers high creditworthy yield and undercollateralized loans to emerging markets. Auditors are randomly selected to check the quality of credit of a new borrower before a loan is added to the platform, this check is designed to avoid any fraudulent applications and auditors will take a vote before any credit is added to the platform. Auditors are rewarded for this process with tokens. To avoid possible "sybil attacks" each participant in the equation needs to pass a unique entity check to prove they are real, once confirmed they will receive a "soulbound token" (non-transferrable NFT) that acts as KYC.

Similar to Centrifuge, Goldfinch also offers different levels of risk for investors. Investors have the possibility to invest in a senior pool which is an automatically diversified pool made up of multiple loans on the platform and the capital acts as a second loss reserve. This means that in the event of a default, repayment is prioritized for the senior pool participants.

Giving users the option of different risk profiles is extremely valuable as different users are likely to have different risk tolerances, this is an important part of onchain RWA as it is important not only to be permissionless but to also be inclusive to all levels of users.

Ondo Finance

Ondo Finance recently launched into the space aiming to bring US Government Bond yield on-chain. The platform allows KYC'd users to deposit stablecoins such as USDC and get tokenized exposure to US government bond yield onchain, the users have the ability to easily enter and exit the government bond position whenever they want. The tokenized position can only be sent to whitelisted addresses and contracts meaning that you cannot freely send the tokens anywhere you wish as Ondo needs to comply with strict KYC regulations.

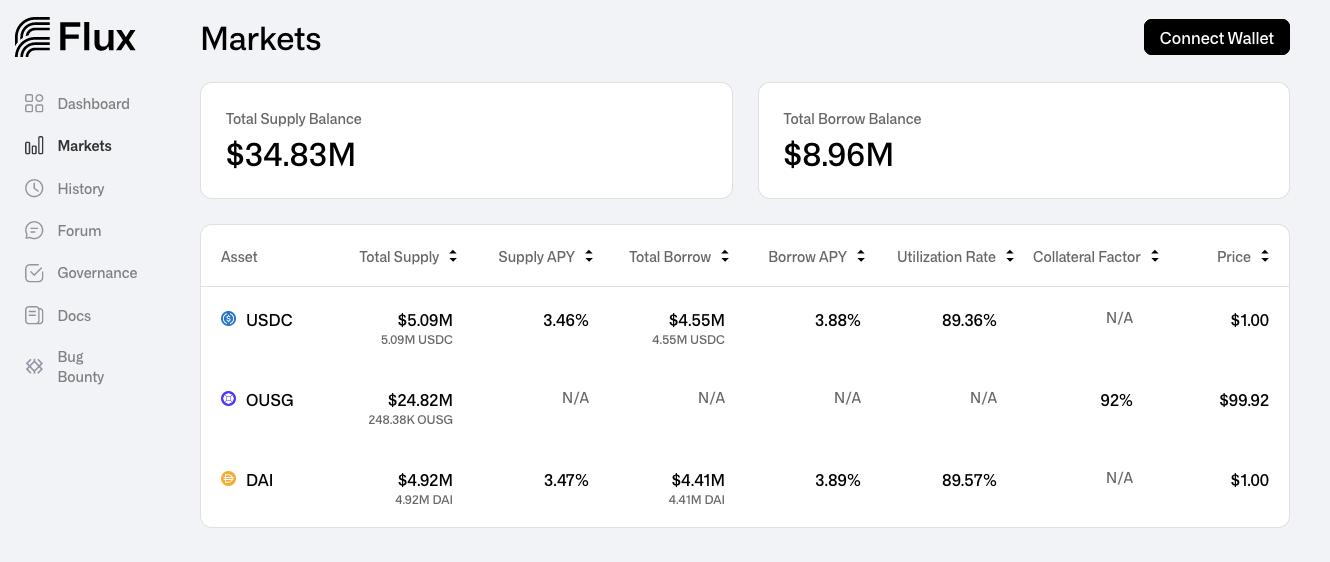

As you would expect not anyone can just buy US Treasuries and the KYC procedure is rather strict meaning that the average degen cannot deposit at Ondo and start earning the juicy yields on their USDC. However, with the help of Flux Finance, this US Treasury yield is synthetically transferred to the broader DeFi market. Flux Finance gives the ability for Ondo users to borrow USDC and DAI against their tokenized US Treasury position and due to the relatively high yield these positions earn they can afford to pay a higher borrow rate and still be profitable. So what this effectively means is that the supply rate for USDC/DAI for the average user is much higher than the rest of the other lending markets in DeFi as the borrower can afford the higher rate, and now the DeFi market has access to synthetic US Government Bond interest rates.

Maple Finance

Maple Finance is an undercollateralized lending platform where users can lend their assets to crypto-native institutions in return for a yield. Unlike Compound or Aave these loans are undercollateralized and credit delegates analyze the quality of the credit before adding it to the platform for users to contribute to. In order for an entity to open a borrow pool on the Maple platform they must undergo KYC/AML checks as well as an analysis of their creditworthiness to assess their profitability and whether they are a fit candidate for a Maple borrow pool.

The theme of undercollateralized lending is an important one to be addressed as without it the crypto lending market can only grow linearly as total borrowing is capped to the total amount of assets put up for collateral and cannot exceed it. In the TradFi world undercollateralized lending is the backbone of many business models (banks) and when done correctly can encourage huge amounts of growth in an economy/ecosystem.

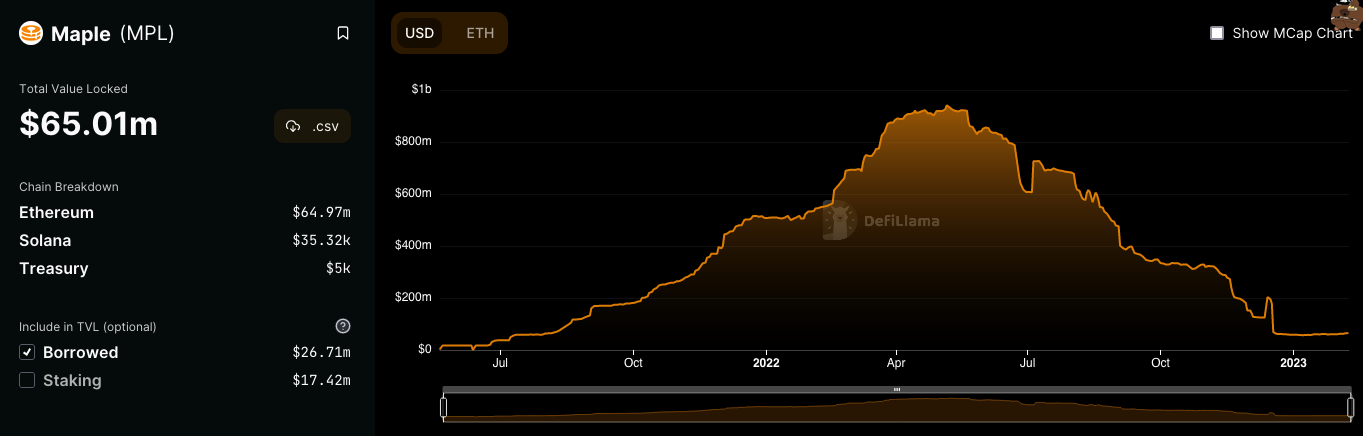

As we can see from the Defillama chart above, Maple Finance experienced an explosion of growth in its lending pools (TVL) at the height of the bull market as liquidity was plentiful and speculation on RWA/undercollateralized lending protocols was rife. While this chart is a familiar pattern for most protocol TVLs, when looking at the RWA space we are seeing many all-time highs in TVL as RWA adoption begins to grow. Another common chart pattern can be seen below, where protocol cumulative incentives and market cap are inverted as vampire capital farms and dumps the protocol rewards, this also part explains the TVL explosion followed by a steady decline.

Out of all of the RWA protocols Maple has unfortunately suffered the most as they experienced a default of around $36m in their lending pools as a result of the FTX crisis. While undercollateralized lending is an important frontier to be conquered we are yet to see a successful attempt.

Maple is not the only party to be the victim of undercollateralized lending gone wrong as we have seen over the past year a slow and painful unraveling of people affected by the crypto credit crunch. Gemini Earn is another current example of how undercollateralized lending can go bad quickly, as their Earn customer's funds are currently stuck in limbo as negotiations between Gemini and Genesis continue.

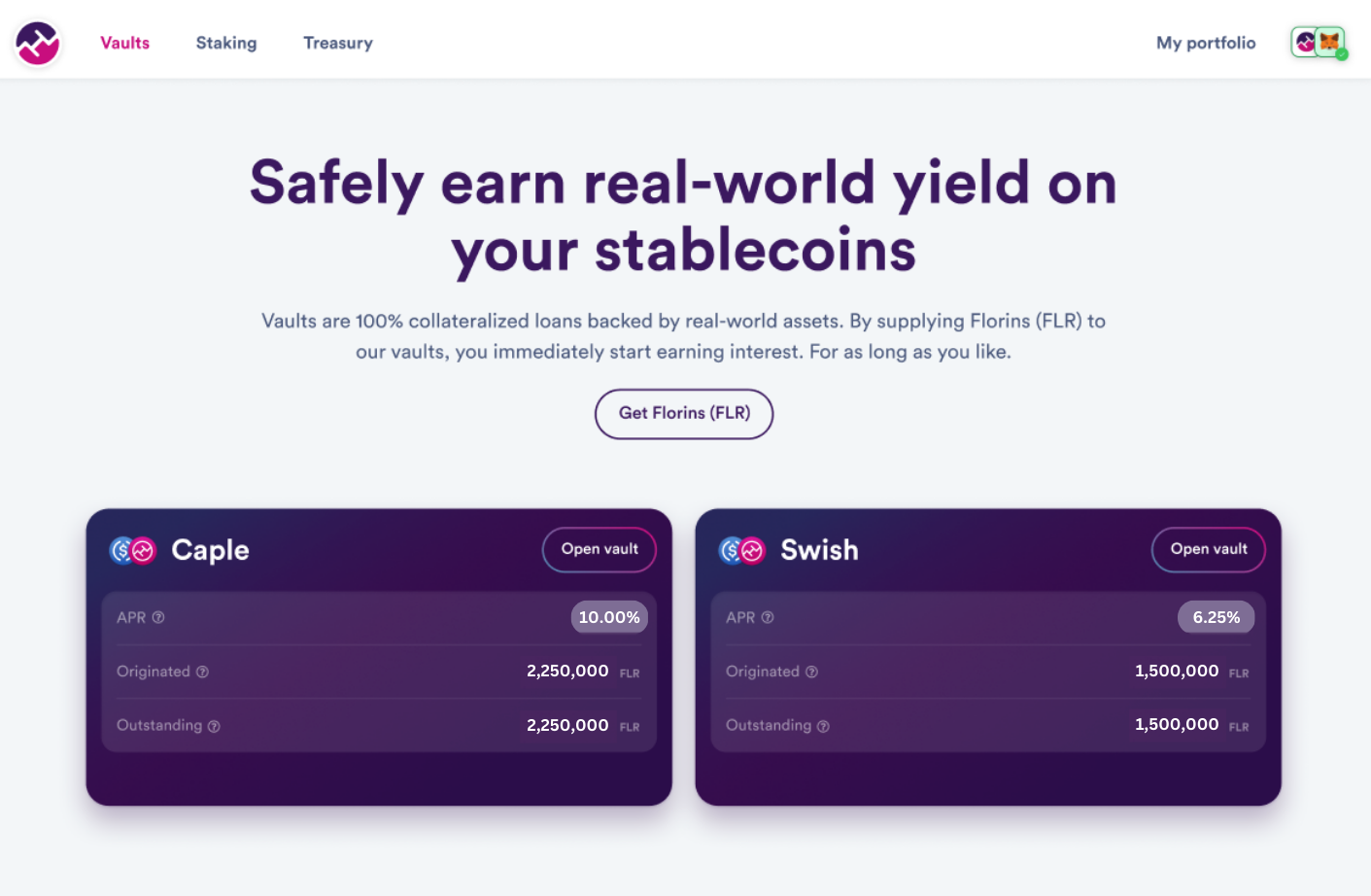

Florence Finance

Florence Finance is an RWA protocol focused on bringing real-world yields on-chain. Addressing the European SME funding gap by providing loans to SMEs in Europe using crypto liquidity such as stablecoins. Florence's approach aims to provide a stable and reliable yield on your crypto that is not dependent on the broader crypto market's performance.

Florence partners with existing SME lending partners and utilizes their expertise to source and manage the best loans for the platform, this means the credit work is outsourced to professionals who have a proven track record. The Florence team also has decades of credit experience which means they are able to check the work of the lending partners and ensure that they are happy with the loans before they are added to the platform, this level of quality control is what should help keep defaults to a minimum.

So far Florence has deployed around €3.75m into active loans with another €3.25m waiting to be deployed to loans. Florence offers various vaults that each offer different APRs depending on their level of risk, the APR varies from 10% for the most Junior vaults and 6.25% for more senior vaults, both paid in stablecoins without any extra token incentives.

Florence Finance focuses on bringing composability to the RWA space as the vault tokens that represent your underlying interest-bearing position could potentially be used as collateral to borrow on another platform similar to the way Centrifuge is integrated with MakerDAO. This means that Florence is giving the ability to other DeFi protocols to add RWA exposure to their platforms and increase their offering to their users.

Conclusion

When looking at TVL or lending/borrowing activity we can see a clear trend of what is currently gaining traction and attracting capital, low-risk uncorrelated sources of real yield that can be funded with onchain liquidity. This can be seen in projects such as Ondo, Maker, Centrifuge, Goldfinch & Florence which all have reached all-time highs in TVL (lending/borrowing activity) during the crypto bear market, reinforcing the RWA narrative as being something here for the long run. While they all approach the RWA space with different methodologies and target markets the underlying thesis is the same, in order for crypto to mature and grow as a whole an underlying pillar of sustainability needs to be constructed as the foundation of the market and bringing real-world assets and yields onchain achieves this.

As we can see there have been various ways protocols have tried to get real-world assets and yields onchain, while we are still in the infant stages of this space where a clear path to adoption is not clear and regulation is still overhanging it is hard to say who will come out on top. But one thing we are sure of is that in order for crypto to achieve mass adoption we will need to bring more real-world assets onchain and build more bridges between the real world and DeFi.