How RWA's broke $100bn in value without anyone noticing

Real-World Assets: Bridging the Gap Between Traditional and Digital Economies

Introduction

The world of cryptocurrency is constantly evolving and what started as a peer-to-peer electronic payment system is now a sprawling ecosystem of developers & users collaborating to build the future of finance & value. The integration of real-world assets into crypto has opened up new avenues for financial innovation and in this article, we explore real-world assets in the realm of cryptocurrency, what they mean for crypto, and the potential they hold for reshaping the global financial landscape.

Defining Real-World Assets

Real-world assets ("RWA's") as used/defined in crypto are simply tokenized versions of existing traditional (mostly financial) assets as opposed to solely/natively digital assets. Such assets can include real estate, precious metals, commodities, and even artworks but in practice, they mostly relate to existing securities (stocks & bonds) and last but not least, currencies a.k.a. stablecoins. It is especially the latter's contribution to TVL that has allowed RWA's to break the $100bn mark. This represents approximately 10% of the value of all digital assets at current prices, but what is less known is that up to 70% of all on-chain transactions (by value - according to Nic Carter) are currently stablecoin-based, up from low double digits a couple of years ago.

Blockchain technology, the foundation of most cryptocurrencies, provides a decentralized, secure, transparent, and immutable ledger for recording ownership and transactions. By tokenizing real-world assets on a blockchain, their ownership can be easily transferred, administered, and traded digitally, enabling a seamless connection between the digital and physical realms of value.

Benefits of Tokenizing Real-World Assets

- Permissionless Accessibility: Tokenization abolishes barriers to entry, allowing a broader range of investors to access assets that were previously reserved for high-net-worth individuals or institutions with access to USD bank & brokerage accounts. Fractional ownership enables investors to buy small portions of valuable assets, promoting inclusivity.

- 24/7/365 Liquidity: Traditional real-world assets can be illiquid, meaning it's challenging to quickly convert them into cash without significant transaction costs or time delays and such conversion is often controlled by centralized parties. Tokenization enhances liquidity by enabling assets to be traded 24/7 on multiple/decentralized exchanges, providing a more flexible and efficient market.

- Instant settlement + full Transparency: Blockchain's instant settlement negates the need for transaction intermediation and 3rd party custody. Transparency and immutability eliminate fraudulent practices and provide a clear audit trail for every transaction. This transparency instills trust among investors and stakeholders.

The Current State of Stablecoins + RWA:

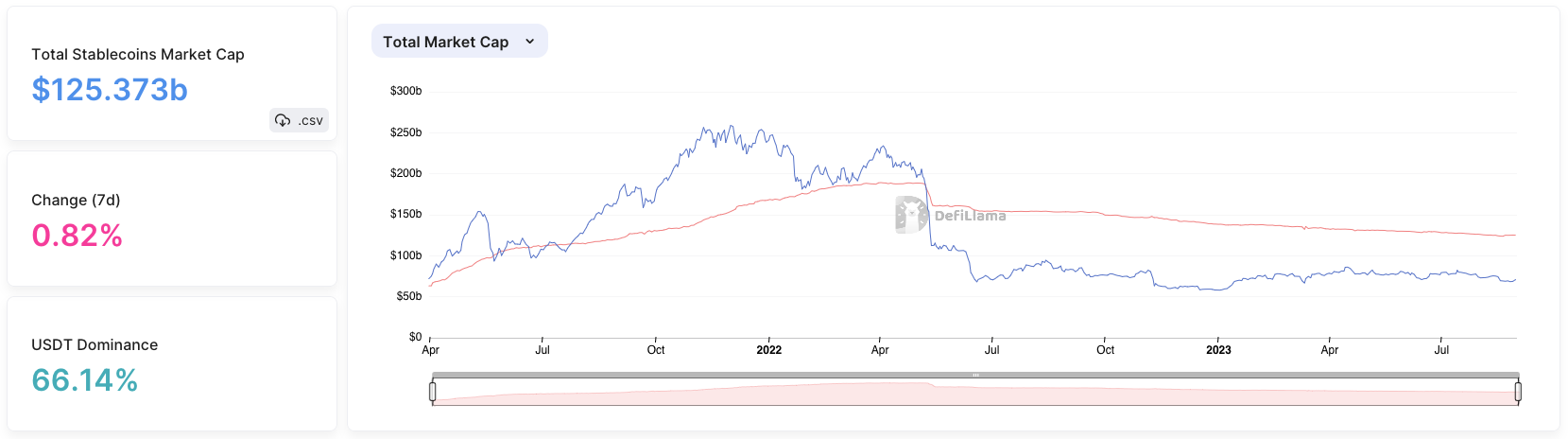

Courtesy of Defillama we can see that the current market cap of all stablecoins is currently sitting at around $125 billion, down from its peak of ~$250 billion in 2021.

There are many projects working hard in the RWA space to bring real-world assets and yield on-chain, as seen in this recent thread by Hercules Defi. Truth be told however, the TVL of non-stablecoin RWA protocols is still tiny in comparison to stablecoins. We would argue that stablecoins are RWAs whether they share the underlying yield or not, the difference being whether the stablecoin is a digital representation of a Government bond or merely its currency. Given most stablecoin issuers already have the majority of their reserves in Government bonds we think it is only a matter of time before they are forced to share the underlying yield, we believe we are halfway there to having more than 100bn of yield-bearing RWA's onchain.

Are Stablecoins the killer application?

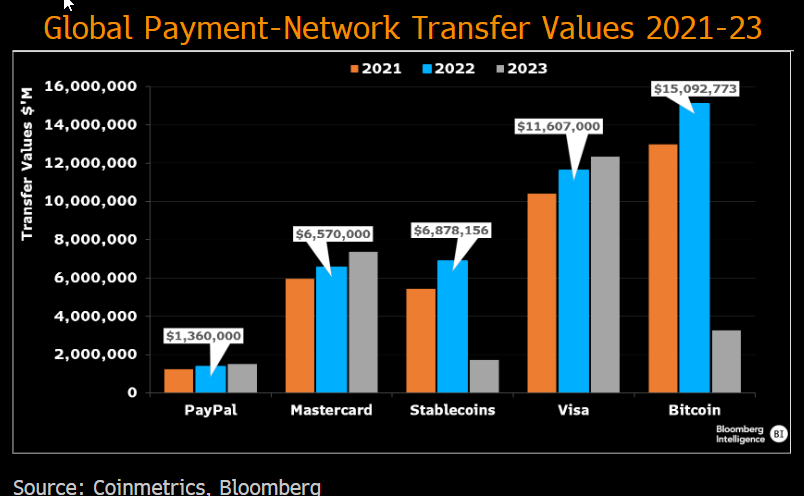

As Jamie Coutts highlighted in a recent Twitter thread (which inspired this broader article), stablecoin payments actually overtook Mastercard in 2022 by volume ($6,9 trillion vs. $6.6 trillion respectively) and easily surpassed the $100bn TVL mark in that same year.

This year, volumes have come down significantly due to reduced (bear-)market activity and hostile US regulators. Clearly indicating that a lot of this volume is trading rather than real-economy payments related.

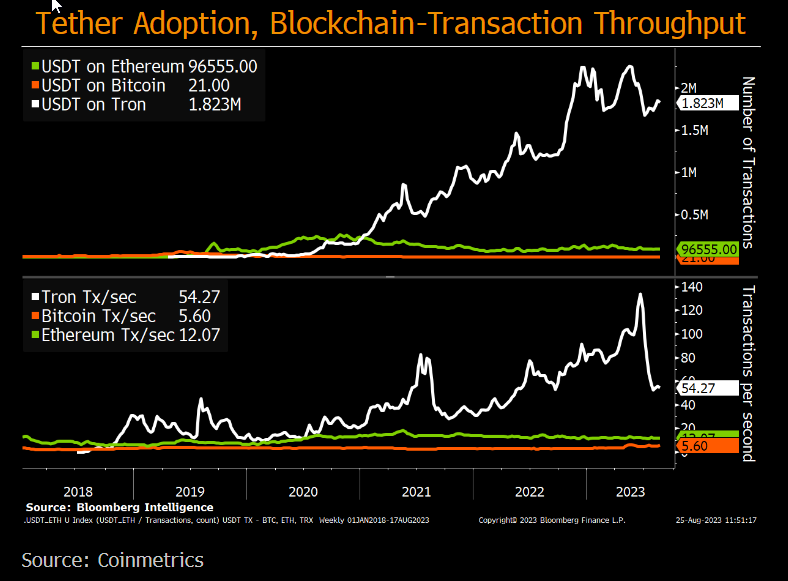

Stablecoins started with Tether (USDT) on the Bitcoin network and have taken a massive flight every time the transaction cost and speed were improved, first on Ethereum, then on Tron, and now on L2's.

Stablecoin issuance was more challenging in a zero/negative interest rate environment. However, the fastest rate hiking cycle in history has now made it one of the most lucrative hustles in crypto with the yield on reserves accruing 100% to the issuer such as Tether and Circle. Given this underlying profitability dynamic and incremental regulatory clarity under MiCA, we expect an explosion of stablecoin issuance as well as a gradual movement to some form of "revenue share" of the windfall interest margin on the back of increased competition.

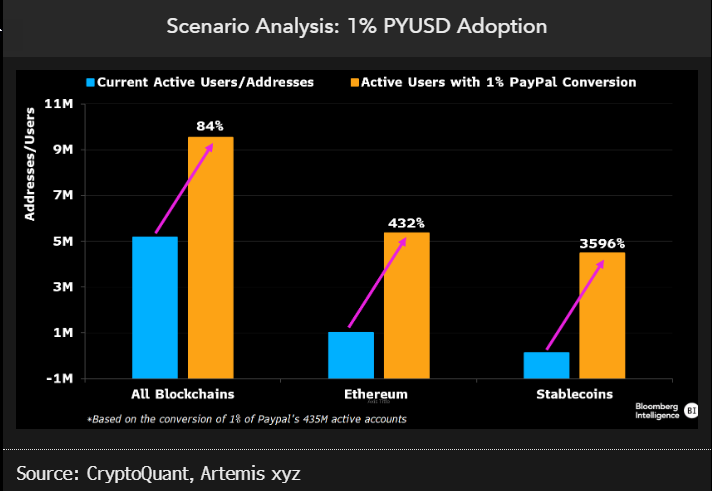

Now that PayPal has decided to launch its own USD stablecoin ($PYUSD) and Twitter (aka X) has acquired a crypto payments license, others are likely to follow and the competition for Circle and Tether is about to heat up enormously in our view.

The potential implications for crypto, especially Ethereum, are huge... If only a small percentage of PYPL users and other normie payment platform users become crypto natives, the stablecoins' overall adoption could double overnight. Add the Twitter users to that and you can start to see how the growth could explode.

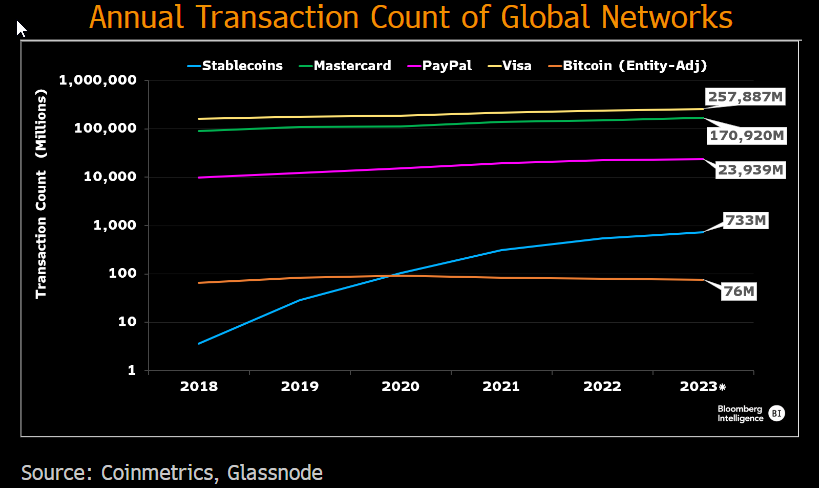

Though this all looks very bullish on paper, it is probably not realistic in the short term given the current L1 transaction speed and gas fees (high transaction costs). So, although transaction growth has been exponential, annual stablecoin transactions are still only 0.5-3% of TradFi payment networks, and the potential for this new money to dominate global payments is still wholly dependent on the ability of public blockchains to address current scaling issues ASAP. We need more transaction throughput at a lower cost to onboard these new users.

Notwithstanding the transaction cost argument limiting market share to date, one should not ignore the stablecoin adoption trend we are seeing. Scaling is improving even in the depths of this bear market, and we think it is possible we are about to reach an inflection point where stablecoins can offer a cheaper alternative to TradFi.

Take Tether as an example. First, it was on the Bitcoin network. History shows stablecoin liquidity and adoption explode once faster & cheaper alternatives appear.

In 2020, Tron began processing more stablecoin transactions and doubled Ethereum in transactions per second. By mid-2023, Tron had increased throughput to 130 transactions per second, more than 10x Ethereum, facilitating almost 20x the number of transactions.

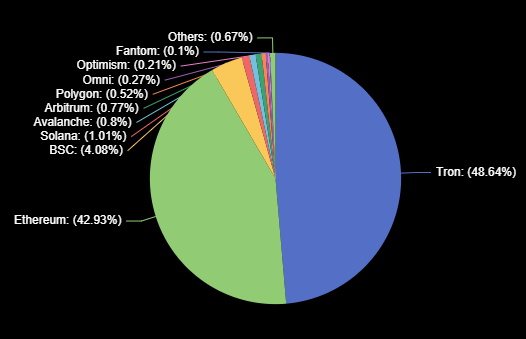

Now we understand Tron is not exactly the poster child for a decentralized and transparent network and that is probably why it hasn't absorbed all of USDT's market cap (48% vs. 42% on ETH), but it does show clearly that transaction speed and cost drive adoption.

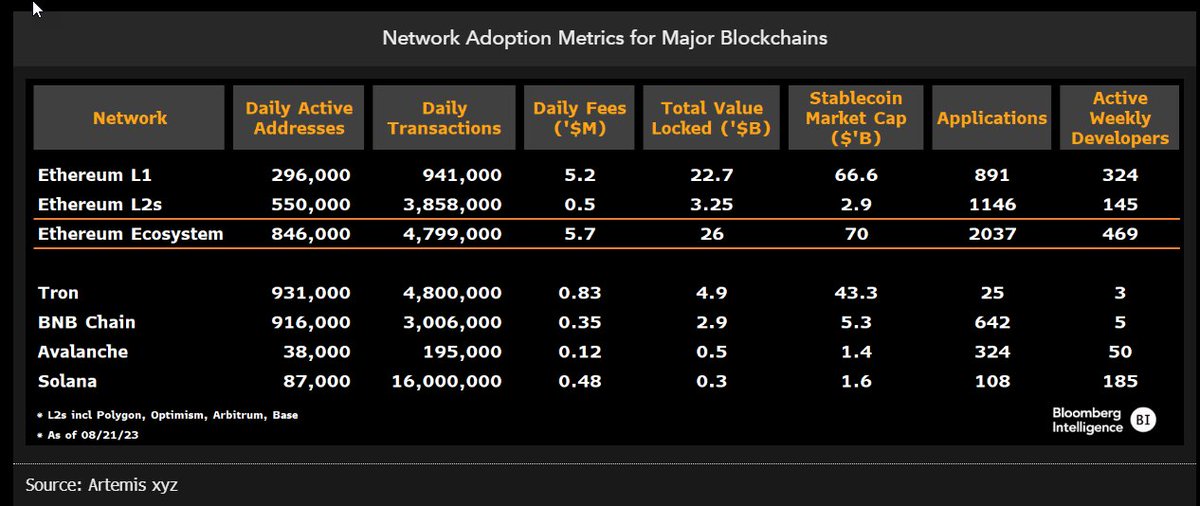

Across most network-adoption verticals, Ethereum and its broader ecosystem of fast-growing rollup chains (L2s) such as Optimism, Base, and Arbitrum, lead all alternative networks and are offering competitive transaction costs and almost instant settlement. That said the BTC lightning network has also been garnering attention lately and who knows maybe others like Solana or newer Rust-based L1/2s still have a chance to take the crown.

All we know is that between the work being done on Lightning and Ethereum's rollup-centric scaling roadmap, there will be L2 transactions that are vastly cheaper than today's benchmarks. Possibly as much as (10-100X) by next year with EIP-4844 (proto-dank sharding) at which point stablecoins will effectively be better on every dimension than TradFi alternatives.

Assuming we can put hostile US regulators and macro headwinds behind us sometime in the near term future, and builders keep building, adoption will explode.

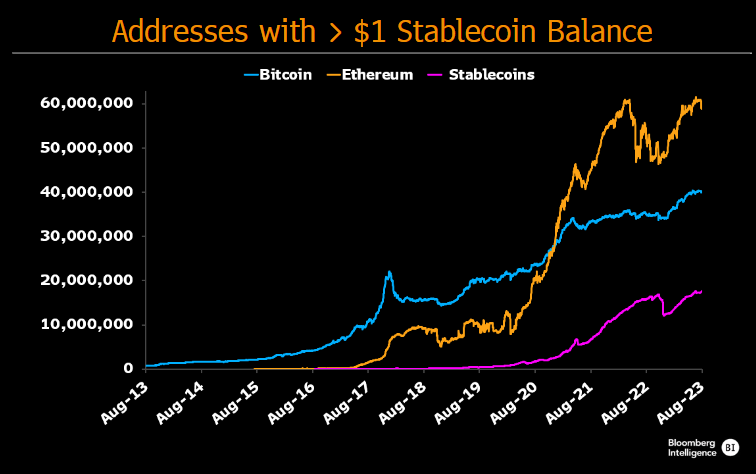

An interesting metric for adoption rather than looking at cyclical volumes is crypto addresses with > $1 balance of stablecoins.

This metric has just hit ATHs ~ 17.4 million. Since 2021, these addresses have outpaced BTC & ETH growth by 7x.

If the current utility is combined with a portion of the underlying yield as transaction costs drop by orders of magnitude, it would appear logical that stablecoins will be the biggest drivers of adoption as the network effects of payment providers and online merchants (e.g. PayPal, Visa, Shopify) take hold.

Musings on issuers & market structure

As stated previously it all started with Tether and the desire for crypto exchanges & market makers to have a crypto native dollar pegged asset for settlement and as a place to be risk-off within crypto. To these people transaction speed and cost mattered less than the fact that it was permissionless (not intermediated). The fact that they weren't being paid interest was at the time no different than their bank given the prevailing zero interest rate environment.

As transaction costs came down and transaction/settlement speeds improved, more and more use cases became viable. With global central banks hiking yields to address inflation worries, early fully reserved issuers (Circle/Tether) treasuries turned into the biggest money makers in crypto. So much so that even decentralization zealots like MakerDAO have caved to the lure of holding reserves in US Government Bonds over decentralized and/or over-collateralized alternatives.

Early attempts at bringing credit creation on-chain have somewhat poisoned the well for RWA's with Block-Fi, Genisis, Celcius, Voyager, and others all falling victim to asset-duration mismatches and other types of (credit-) mismanagement. It is however too soon in our opinion, to throw the on-chain credit baby out with the bathwater as these initial failings were at least in part endemic and thus solvable with RWA's. On-chain lenders could only lend to crypto-native borrowers as many of the crypto firms were (and still are) being denied access to TradFi banking & lending markets. This meant that on-chain lending and borrowing was largely within the crypto ecosystem (i.e. endemic). Herein lies the problem: If you are lending to an ecosystem that is trading-centric & highly leveraged, and the underlying assets have volatility multiples much higher than that of traditional markets, the cashflows and collateral tend to be much too volatile to run credit books against safely. The result of which was as painful as it was pre-ordained.

Enter RWA's. With real-world credit exposure and collateral that is less volatile, you can start to imagine a world where on-chain credit actually enhances the ecosystem by providing a means to diversify risk away from the volatile underlying crypto native assets. That said, in a world where Governments are currently paying you NOT to do any credit work (i.e. why lend to a corporation or an SME when I can get 5.5% risk-free), it is easy to understand the allure of simply keeping on-chain reserves in Government bonds. Hence, the currently prolific attempts at effectively bringing Government bond yields on-chain (Ondo Finance, Maker, Maple et al.). Although we can understand the incentive and allure of this, it is also the epitome of what is wrong with the TradFi financial system. As Arthus Hayes also recently alluded to in his newsletter, if banks are incentivized to park their money in treasuries or at the FED, real economy credit creation suffers. I would go so far as to say that with current fiscal largesse and regulatory capture of the TradFi system, real credit creation is doomed as Governments crowd out the private sector in an ever-increasing manner.

It is for this reason that we started Florence Finance and that we are firm believers in the "real economy" part of Real World Asset protocols such as Centrifuge, GoldFinch, BlueJay & our own. Fully reserved stablecoin issuers such as Tether & Circle will continue to have a role but will likely morph to become either tokenized versions of central bank reserves (MiCA model that requires all reserves to be held at the Central Bank) or effectively tokenized Money Market Funds. These both already exist in the TradFi system but will be more efficient & transparent on-chain. As they are integrated into more and more payment platforms they will further exasperate the "slow walk" of deposits out of the banks into these on-chain alternatives with higher utility and higher yield. The real innovation however we think will be in the grassroots decentralization of real-world credit creation away from TradFi as they become more and more ensnared in the financing of fiscal largesse and unable to compete with leaner decentralized (preferably non-fractionally reserved and therefore less regulated) alternatives.

Conclusion

The integration of real-world assets into the crypto space represents a significant step toward merging traditional and digital economies. Tokenized assets offer increased accessibility, liquidity, and transparency (read utility) and potentially higher yield. As the technology and market mature, tokenized real-world assets will reshape the financial landscape, democratizing credit creation & investment opportunities and drive crypto's next adoption cycle.

Florence Finance fixes this...