The last bank run

Over the last year, you will most likely have seen the words "Bank Run" thrown around when Terra Luna and FTX collapsed and now it is coming closer to home with even TradFi banking institutions (SVB, First Republic, and Credit Suisse) suffering similar fates. But what is a bank run?

"A bank run occurs when a large number of customers of a bank or other financial institution withdraw their deposits simultaneously over concerns of the bank's solvency"

If a bank receives withdrawal requests in excess of the (small) fraction of its balance sheet that it keeps in liquid assets (cash & short-term government securities) to meet such withdrawal requests in the ordinary course, the bank has to throttle/limit its payouts to such withdrawal requests causing even more people to want to withdraw their funds. Such a liquidity-induced crisis need not be catastrophic as long as the bank can (in time) raise the funds required to honor all withdrawals. If however, the liquidity situation forces the bank to liquidate assets at below book value it can very quickly lead to actual insolvency (i.e. the bank's assets are worth less than its liabilities). This is exasperated by the leveraged and fractionally reserved nature of the TradFi banking system in combination with not MTM their "hold to maturity" asset portfolios. This is why we invented Central Banks, their role is to backstop such scenarios & risks (i.e. lend endlessly against good collateral) and we have depositor's insurance schemes to provide assurances around such backstops to prevent bank runs from happening in the first place.

All that said it is pretty clear from the discourse ongoing on Twitter that the traditional Central Bank tools and rhetoric are not quite up to the task of maintaining stability in a system that is driven by lighting fast spread of information via social media platforms in combination with enhanced investor and depositor access to deposits and alternative asset classes (Money Market Funds or indeed Crypto) at the click of a button.

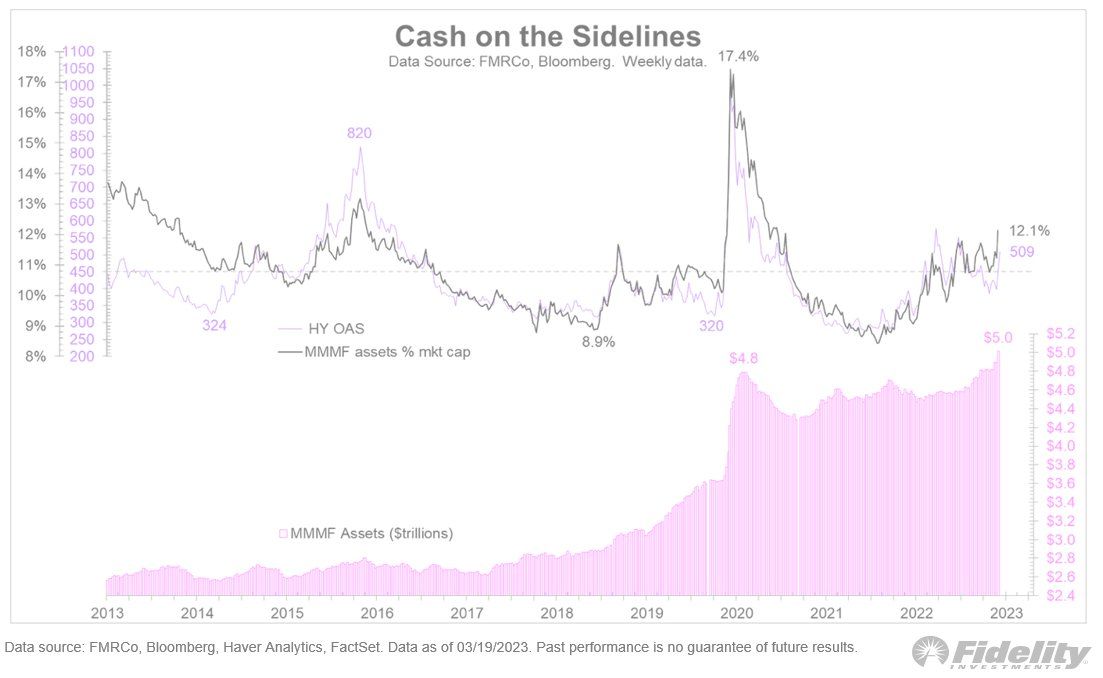

What was announced as a 25bn FDIC insured backstop (the BTFP), quickly became a 300 billion increase of the FED balance sheet in the first week of the program's existence, rumored to grow to 2tr (that's trillion with a T). At the time of writing the speculation is rampant that even this will not suffice, and the FED will have to backstop all deposits - a full $18 trillion!

This is obviously bordering on the absurd, but it is the inevitable direction of travel for a system that is over-levered at every level; whether that be at the personal level, the corporate level, the bank level, or indeed the Governments/nations themselves.

I was personally never convinced of the hyperbitcoinization thesis and if history shows anything it is that, the powers are very good at kicking the proverbial can down the road. That said, I think the realization that the system is too fragile and inherently unstable is starting to seep through into the collective cognizance and rational actors are starting to act in a manner that will force the system to auto-correct. Balaji's 1 million dollar bet on BTC is a call to arms to effect such change and a just cause from that perspective.

In crypto, there is no Central Bank and thus the occurrence of a bank run poses a much greater risk (Bitfinex 2019, Tether, Celcius & BlockFi etc. in 2022) and thus crypto institutions need to maintain higher liquidity and hold themselves to higher standards. Unfortunately, few of the parties identified above did just that at the time of failure. Their failures and/or losses however have contributed to the remaining players learning that very valuable lesson. Circle was able to re-establish its peg after failure (over the weekend on the back of SVB closure) relatively quickly once the settlement was resumed on Monday on the back of ample and liquid reserves.

In TradFi, Central Bank interventions are having the opposite effect. Not reducing leverage or risk-taking by allowing parties to lend against collateral at par, not holding parties responsible for wrongdoing, etc. This will ultimately result in more and more blow-ups, causing more and more capital to doubt the sustainability of that failing system as the confidence in the less leveraged and more transparent blockchain-based alternatives grows.

The other topic of interest is fully reserved banking intermediaries. I have to say the fully reserved banking "penny" took some time to drop in my head, but now that we have seen that the FIAT on/off ramps and the settlement networks (Signet & SENS) actually being potential points of failure for the crypto system it is clear that we need a fully reserved intermediary as the risks posed by fractional reserves and/or leverage in TradFi are simply not worth it.

Why does all this matter I hear you ask, and can Florence Finance have a "bank run"? In short, there can never be a bank run on Florence, as all participants know there is no liquidity other than through secondary markets. That said, as there is also no leverage in our protocol the chances of it becoming insolvent are practically zero and this is verifiable in a trustless manner at any point in time.

We believe in a tokenized future where customers will be free to move their self-custodial assets/funds freely between various yield or capital gains generating assets/protocols with minimal need for trusted intermediaries.

At Florence Finance our job is to convert users' excess stablecoin balances to yield generating loan exposure to European SMEs in the most efficient and transparent manner possible. To provide a platform for collaboration between users and SME lenders to produce steady/safe/transparent real-world yield on excess stablecoin balances. Because our protocol can verifiably never loan out more than we raise in funding, it has zero leverage and no fractional reserves. Due to the nature of our business model, a bank run may result in people not being able to exchange their FLR for stablecoins temporarily but it can never make Florence Finance insolvent as once we have made a loan to an SME lender those funds are essentially locked until the maturity of the loan. While there may be a temporary lack of third-party liquidity that supports users swapping their FLRs for stablecoins on a DEX, this availability of third-party liquidity has no impact on the actual protocol or the underlying loan portfolio as FLRs are algorithmically and verifiably always backed 1:1 by underlying loan exposure no matter what.

This is very similar to what we see with Lido's Staked ETH (stETH). While stETH trades on various DEXs and can experience liquidity issues causing the price to temporarily stray from its redeemable value (1:1), Lido Staked ETH will eventually be redeemable 1:1 for ETH when withdrawals are open. This is the same for Florence Finance, while the value on a DEX of FLR may fluctuate due to demand/liquidity availability, Florin will ALWAYS be backed 1:1 by underlying EUR loan exposure.